Letter of Demand

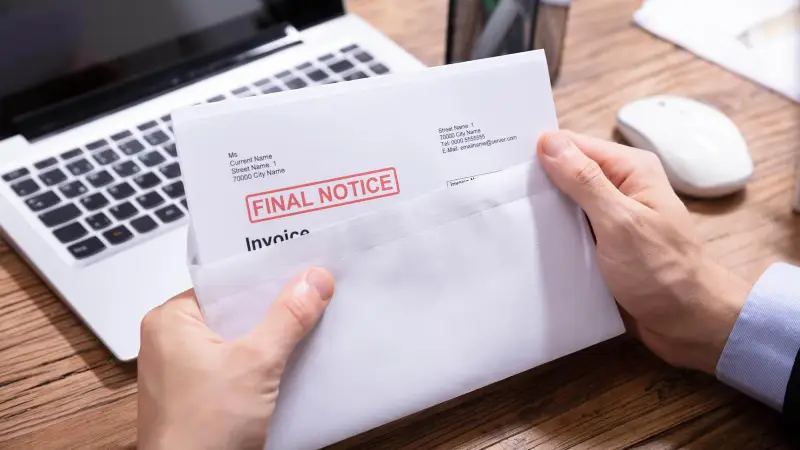

Debt collection letters play a crucial role in the debt recovery process, especially in New Zealand’s legal and business landscape. These letters serve as formal notifications, alerting individuals or businesses that they have an outstanding debt that needs to be settled. Whether it’s a reminder for an overdue invoice or a final notice before legal action, a debt collection letter is often the first step in reclaiming unpaid funds.

Understanding the different types of debt collection letters, including the letter of demand template NZ, how they work, and the legal implications behind them can help both businesses and consumers navigate the often-complicated world of debt recovery. For businesses, sending the right type of collection letter, such as using a letter of demand template NZ, can make the difference between recovering funds promptly and facing prolonged financial losses. On the other hand, for individuals receiving these letters, knowing their rights and obligations can help them avoid unnecessary legal action and further financial strain.

In New Zealand, debt collection letters must comply with certain laws and regulations to protect consumers while ensuring businesses have the tools they need to recover what they are owed. This article will delve into the various types of debt collection letters—such as debt recovery letters, formal debt collection letters, and lawyer debt collection letters—and their significance in the New Zealand market. Through real-world examples, case studies, and practical templates, this guide aims to equip you with the knowledge and tools to effectively deal with debt collection matters, whether you’re sending or receiving a debt collection letter.

In the following sections, we’ll explore the different types of debt collection letters, their purpose, legal considerations, and how to approach them.

Key Sections :

What is a Debt Collection Letter?

A debt collection letter is a formal written notice sent by a creditor, collection agency, or attorney to an individual or business that owes money. Its primary purpose is to inform the debtor of their outstanding balance and demand repayment within a specific period. Debt collection letters are an essential part of the debt recovery process, offering a clear, documented communication path between the creditor and debtor.

In New Zealand, these letters are governed by regulations that protect both parties. The letter serves not only as a reminder but also as a legal record that the creditor has made an effort to collect the debt before pursuing more serious actions like court proceedings or hiring a solicitor. A well-crafted debt collection letter can often resolve payment disputes without the need for further escalation.

Key Components of a Debt Collection Letter

A typical debt collection letter contains:

- Creditor Information: Clearly identifies the company or individual owed money.

- Debtor Information: Specifies the name and address of the person or business responsible for the debt.

- Debt Details: Outlines the amount owed, due dates, and any interest or fees accrued.

- Payment Instructions: Provides the debtor with details on how to make the payment, including accepted methods and deadlines.

- Consequences of Non-Payment: Explains what will happen if the debt is not paid, such as further action like sending the debt to collections, legal proceedings, or additional fees.

Example:

Imagine a small business in Auckland that has been owed $1,500 for over three months by a client. The business sends a debt collection letter that outlines the overdue amount, provides a final deadline for payment, and warns that failure to comply will result in legal action. The letter includes all the required details to ensure the debtor understands their obligations and the potential consequences of non-payment.

Different Types of Debt Letters

There are various types of debt letters, each serving a unique purpose:

- Collection Letter: A general term used for any letter sent to request payment of a debt.

- Debt Recovery Letter: Used when a creditor is trying to recover an outstanding balance that has been overdue for an extended period.

- Debt Collection Notice: A more formal notice, often indicating the final step before sending the debt to collections or taking legal action.

- Debt Collection Letter of Demand: A stronger form of the debt collection letter that explicitly demands payment and warns of the immediate consequences of non-payment, including legal action.

Sample Scenario:

A local construction company in Wellington is trying to recover unpaid invoices for completed projects. After multiple informal attempts to contact the client, they send a debt collection letter of demand, stating that if payment is not received within 14 days, the debt will be sent to a collection agency.

When Should You Send a Debt Collection Letter?

Knowing when to send a debt collection letter can significantly impact its effectiveness. Generally, businesses wait until an invoice is at least 30 days overdue before sending the first collection letter. However, if the debt remains unpaid after the initial reminder, follow-up letters, such as a formal debt collection letter, should be sent.

Each debt collection letter should escalate in urgency, moving from polite reminders to more assertive demands, particularly when there is no response from the debtor. In many cases, a well-timed letter can prompt immediate payment without the need for further action.

In the next section, we will explore the various types of debt collection letters more deeply, including how to tailor them to specific situations.

Types of Debt Collection Letters

Debt collection letters come in various forms, each designed to address different stages of the debt recovery process. Depending on the debtor’s response (or lack thereof), the letters can range from gentle reminders to final demands before legal action. Below, we break down the different types of debt collection letters, their purposes, and when to use them in the New Zealand context.

1. Debt Collection Letter of Demand

A debt collection letter of demand is often considered one of the most assertive steps in the collection process. This type of letter is usually sent when previous attempts to collect the debt have failed, and it serves as a final warning before the creditor escalates the issue to legal action or a collection agency. The letter outlines the amount owed, provides a deadline for payment (typically 7 to 14 days), and warns that failure to comply may result in court proceedings.

Example:

A small retail business in Christchurch is owed $5,000 by a supplier who has not paid their outstanding invoices for over 90 days. After several unsuccessful attempts to recover the debt, the retailer sends a debt collection letter of demand, stating that if payment is not received within 14 days, legal action will be pursued.

Sample Debt Collection Letter of Demand:

Dear [Debtor's Name],

This letter serves as a final demand for the outstanding payment of $5,000 for the goods supplied on [Date]. Despite previous reminders, we have not received the payment. Please arrange for full payment within 14 days of the date of this letter.

Failure to do so may result in us taking legal action to recover the debt, which could include additional costs for legal proceedings.

Kind regards,

[Your Name]

[Your Company]2. Collection Letter

A collection letter is a general notice sent to remind the debtor of their unpaid balance. Unlike the more assertive debt collection letter of demand, a collection letter is typically used early in the process and serves as a polite reminder that payment is due.

Example:

A digital marketing agency in Auckland sends a collection letter to a client who has not paid their invoice for services rendered. The letter gently reminds the client of the outstanding payment and offers them a grace period to settle the balance.

Sample Collection Letter:

Dear [Debtor's Name],

We hope this letter finds you well. We would like to remind you that your payment for the services provided on [Date] is now overdue. The total amount due is $1,200.

Please arrange payment within the next 7 days to avoid further reminders.

Thank you for your prompt attention to this matter.

Best regards,

[Your Name]

[Your Company]3. Debt Recovery Letter

A debt recovery letter is typically sent when a creditor is trying to recover a debt that has been overdue for an extended period. This letter is more forceful than a basic collection letter but still allows the debtor an opportunity to settle their account before more serious measures are taken.

Example:

An IT service provider in Hamilton has been waiting six months for payment from a client. They send a debt recovery letter, which emphasizes the need for immediate payment and the potential consequences of continued non-payment.

Sample Debt Recovery Letter:

Dear [Debtor's Name],

This is a notice that your account has been overdue for six months. We have previously contacted you regarding this matter, and no payment has been received.

Please arrange for immediate payment of $2,500 to avoid the need for further action.

Sincerely,

[Your Name]

[Your Company]4. Formal Debt Collection Letter

A formal debt collection letter is a more serious notice, often used after multiple reminders have gone unanswered. This letter clearly states the consequences of non-payment, such as escalating the matter to a collection agency or solicitor. It may also include the legal costs that the debtor could incur if the case is taken to court.

Example:

A law firm in Wellington sends a formal debt collection letter to a client who has ignored several previous notices. This letter serves as the final warning before legal proceedings commence.

Sample Formal Debt Collection Letter:

Dear [Debtor's Name],

We regret to inform you that your payment of $3,800 for services provided on [Date] remains outstanding. Despite our previous attempts to contact you, no payment has been made.

We must now inform you that unless full payment is received within 10 days, we will have no option but to escalate this matter to legal proceedings, which may include additional legal costs.

Please take immediate action to resolve this issue.

Sincerely,

[Your Name]

[Your Company]5. Collection Letter from Attorney

A collection letter from an attorney adds a layer of legal seriousness to the debt recovery process. When a debtor receives such a letter, they understand that the creditor is prepared to take legal action if the debt is not resolved.

Example:

A consultancy firm in Dunedin hires a solicitor to send a collection letter from an attorney to a client who has consistently ignored payment requests. This letter signifies that legal proceedings are imminent if the payment is not made.

Sample Collection Letter from Attorney:

Dear [Debtor's Name],

This letter serves as formal notice that our client, [Your Company], is seeking immediate payment of $4,500 for services rendered. As their legal representatives, we are prepared to pursue this matter through the courts if payment is not received within 14 days.

Failure to settle this debt will result in further legal action, including additional costs for court proceedings and legal fees.

Sincerely,

[Attorney's Name]

[Law Firm]6. Payment Collection Letter

A payment collection letter is used to confirm the payment terms and demand the final balance. It often highlights the due date and explains the next steps if payment is not received, such as additional fees or interest.

Example:

A car dealership in Rotorua sends a payment collection letter to a customer who still owes $10,000 on their purchase. The letter clearly states the due date for the remaining balance and outlines the consequences of non-payment.

Sample Payment Collection Letter:

Dear [Customer's Name],

We are writing to remind you that your final payment of $10,000 for the purchase of [Car Model] is due on [Due Date].

Please ensure that this payment is made by the specified date to avoid any additional fees or interest charges.

Thank you for your attention to this matter.

Sincerely,

[Your Name]

[Your Company]In the next section, we will dive deeper into the legal aspects of debt collection in New Zealand, including how to write and respond to legal letters such as the solicitor’s debt collection letter and the debt clearance letter.

Legal Aspects of Debt Collection in New Zealand

Debt collection in New Zealand is governed by strict laws and regulations that ensure both creditors and debtors are treated fairly throughout the process. When drafting or responding to a debt collection letter, it is essential to understand the legal requirements that govern these communications to avoid legal disputes or breaches of consumer rights.

In this section, we’ll explore the legal aspects of debt collection, focusing on the importance of compliance, how to properly handle disputes, and the role of legal professionals such as solicitors and attorneys in the process. Understanding these aspects is crucial for businesses and individuals alike, especially when dealing with more formal legal letters for debt collection or navigating the complexities of the debt collection notice.

1. Legal Letters for Debt Collection

In many cases, when a debt remains unpaid after several attempts to collect, the creditor may turn to legal professionals, such as solicitors, to send more formal and legally binding notices. These notices include solicitor’s debt collection letters and attorney debt collection letters, which serve to notify the debtor that legal action is being considered or will be pursued if payment is not made.

Example:

A manufacturing company in Auckland has tried multiple times to collect payment from a client. After all their efforts have been ignored, they enlist the help of a solicitor who drafts and sends a solicitor’s debt collection letter on their behalf. The letter explains that the company intends to file a claim with the court if the debt is not settled within the next 10 days.

Sample Solicitor’s Debt Collection Letter:

Dear [Debtor's Name],

We are writing on behalf of our client, [Your Company], to demand payment of the outstanding debt of $6,500. Despite multiple requests, this amount remains unpaid.

Please be advised that failure to pay the full amount within 10 days of the date of this letter will result in legal action being taken against you. Our client is prepared to take this matter to court, which may result in further legal costs being added to the debt.

We strongly encourage you to resolve this matter promptly.

Yours sincerely,

[Solicitor's Name]

[Law Firm]2. Debt Collection Notice and Legal Collection Letters

A debt collection notice is a formal communication that informs the debtor of the creditor’s intent to escalate the matter to legal proceedings if payment is not made. This notice usually follows a series of reminders and debt chasing letters and represents a final opportunity for the debtor to settle the debt before legal action is initiated.

Legal collection letters, such as those sent by solicitors or attorneys, hold more weight than standard collection letters because they often outline the specific legal consequences of continued non-payment. These letters may mention court action, bankruptcy proceedings, or garnishment of wages, depending on the severity of the case.

Example:

A property management company in Wellington sends a debt collection notice to a tenant who has consistently failed to pay rent. The notice outlines the legal steps that will be taken, including eviction and a court claim for the unpaid rent, if the balance is not paid in full within 14 days.

Sample Debt Collection Notice:

Dear [Debtor's Name],

This letter serves as a final notice that you have an outstanding debt of $3,000 for unpaid rent. If payment is not received within 14 days, we will begin legal proceedings, which may result in eviction and a court claim for the total amount owed, plus any additional legal fees incurred.

Please contact our office immediately to arrange payment and avoid further action.

Sincerely,

[Your Name]

[Your Company]3. Legal Protections for Debtors in New Zealand

While creditors have the right to recover outstanding debts, debtors are protected by laws such as the Fair Trading Act and the Credit Contracts and Consumer Finance Act (CCCFA) in New Zealand. These laws ensure that debt collection practices are fair, transparent, and respectful of the debtor’s rights.

Key protections for debtors include:

- Fair Debt Collection Practices: Creditors and collection agencies must adhere to ethical practices, ensuring that harassment, threats, or misleading communication are not used to recover debts.

- Debt Dispute Rights: Debtors have the right to dispute the debt and request a debt validation letter from the creditor or collection agency, which verifies that the debt is valid and owed.

- Cease and Desist Letters: Debtors can issue a cease and desist letter to a debt collector, requesting that all communication related to the debt be stopped. This is often used when a debtor believes that they are being harassed or that the debt is not valid.

Case Study:

A customer receives a debt collection letter from a collection agency but believes the debt is not valid. They issue a dispute letter for collections and request a debt validation letter from the agency. The collection agency is legally obligated to provide proof that the debt exists and is owed. If they fail to do so, the collection efforts must cease.

4. Handling Legal Disputes and Debt Dispute Letters

If a debtor disputes the debt, they may respond with a dispute letter for collections or a debt dispute letter. This is a formal written notice to the creditor or collection agency, indicating that the debtor disagrees with the amount claimed or the validity of the debt itself. In response, the creditor must verify the debt by providing supporting documentation, often in the form of a debt validation letter.

When dealing with legal disputes, it’s essential to maintain open communication and provide all necessary documentation to resolve the issue. For businesses, keeping accurate records of all transactions, invoices, and correspondence can be crucial in defending against disputes.

Sample Debt Dispute Letter:

Dear [Collection Agency],

I am writing to dispute the debt associated with account number [Account Number]. I believe this debt is not valid, and I request that you provide me with a **debt validation letter** that includes evidence of the original contract and any charges applied.

Until the debt is validated, I request that all collection efforts be paused.

Sincerely,

[Your Name]

[Your Address]5. Solicitor’s Debt Collection Letters

In more complex cases, especially those involving large sums or extended periods of non-payment, solicitors often step in to handle debt collection on behalf of their clients. A solicitor’s debt collection letter adds weight to the situation, signaling to the debtor that the matter has escalated and legal action may be imminent.

Solicitors typically send these letters when previous attempts by the business or collection agency have failed. This letter may outline specific legal consequences, such as the initiation of court proceedings or even bankruptcy action in severe cases. It’s crucial for both creditors and debtors to understand the seriousness of a solicitor’s involvement and to act accordingly.

6. Debt Clearance Letters

A debt clearance letter is typically sent after the debt has been fully paid off. It confirms that the debtor has satisfied their financial obligation and that no further action will be taken. This letter can be important for the debtor to retain as proof that the debt has been settled in full, and it can help improve their credit rating.

Example:

After paying off a long-standing loan, a debtor receives a debt clearance letter from the collection agency, confirming that the balance has been cleared and no further payments are due.

Sample Debt Clearance Letter:

Dear [Debtor's Name],

We are pleased to confirm that your outstanding debt of $5,000 has been fully paid as of [Date]. No further payments are due, and your account has been closed.

Thank you for resolving this matter.

Sincerely,

[Your Name]

[Your Company]In the next section, we will discuss strategies for businesses to send effective collection letters to customers and ensure compliance with New Zealand’s debt recovery regulations. We’ll also explore best practices for sending payment collection letters and past due collection letters to maintain a positive business relationship while recovering outstanding debts.

Sending Collection Letters to Customers

For businesses in New Zealand, sending effective collection letters to customers is a critical part of maintaining cash flow and ensuring that overdue payments are addressed professionally and promptly. The key is to balance firmness with diplomacy, ensuring that customers are aware of their obligations while preserving the business relationship.

In this section, we’ll cover best practices for sending different types of collection letters, including payment collection letters, past due collection letters, and accounts receivable collection letters. We’ll also explore how to escalate letters if the debt remains unpaid, while still maintaining compliance with New Zealand’s debt collection regulations.

1. Best Practices for Sending Collection Letters

When sending a collection letter to a customer, it’s important to follow some basic principles:

- Clarity: Be clear about the amount owed, the due date, and any potential late fees.

- Tone: Start with a polite, professional tone. Initial collection letters should be written in a way that encourages repayment without damaging the relationship.

- Follow-Up: If no response is received after the first letter, escalate the tone in subsequent letters. Begin with gentle reminders and progress to more formal demands if necessary.

- Documentation: Keep detailed records of all communications, including the dates letters are sent and any responses received. This documentation can be vital if legal action becomes necessary.

Example:

A landscaping business in Queenstown sends an initial payment collection letter to a customer who is 30 days late on their payment. The letter is polite but firm, reminding the customer of the overdue balance and providing instructions for making the payment.

Sample Payment Collection Letter:

Dear [Customer's Name],

We hope this message finds you well. We would like to remind you that your payment of $800 for landscaping services provided on [Date] is now overdue by 30 days. Please arrange payment as soon as possible to avoid any late fees.

If you have already sent the payment, please disregard this notice. We appreciate your prompt attention to this matter and look forward to continuing our work together.

Sincerely,

[Your Name]

[Your Company]2. Past Due Collection Letters

A past due collection letter is usually sent after an invoice has gone unpaid for a significant period, often 60 days or more. This type of letter escalates the urgency and outlines the consequences of continued non-payment. While it should still be professional, a past due collection letter typically includes a stronger request for immediate payment.

Example:

A catering company in Christchurch sends a past due collection letter to a customer who has failed to pay for services rendered two months ago. The letter makes it clear that further delays will result in additional action, possibly involving a collection agency.

Sample Past Due Collection Letter:

Dear [Customer's Name],

We are writing to notify you that your account remains past due. As of today, your payment of $1,200 for catering services provided on [Date] is 60 days overdue.

Please make full payment immediately to avoid additional fees or the involvement of a collection agency. If you are unable to make the payment in full, please contact us to discuss possible payment arrangements.

Thank you for your prompt attention to this matter.

Sincerely,

[Your Name]

[Your Company]3. Accounts Receivable Collection Letters

An accounts receivable collection letter is used by businesses to recover overdue payments from customers. This letter is often part of a company’s routine process for managing accounts receivable and is sent at various stages of the payment timeline. The letter clearly outlines the amount owed and typically offers options for payment, such as a payment plan, if the customer is experiencing financial difficulties.

Example:

A gym in Auckland sends an accounts receivable collection letter to a member who has not paid their membership fees for three months. The letter reminds the member of their outstanding balance and provides instructions on how to settle the account.

Sample Accounts Receivable Collection Letter:

Dear [Member's Name],

We are writing to remind you that your membership fees for the months of [Month], [Month], and [Month] are now overdue. Your outstanding balance is $450.

Please arrange payment by [Due Date] to bring your account up to date and avoid any service disruptions. If you are unable to make the full payment at this time, please contact us to discuss payment options.

We appreciate your prompt attention to this matter.

Sincerely,

[Your Name]

[Your Company]4. Escalating the Collection Process

If a customer fails to respond to initial collection letters, it may be necessary to escalate the matter. This can involve sending a formal debt collection letter, issuing a debt collection notice, or enlisting the help of an attorney or solicitor. These letters are more assertive and clearly outline the legal consequences of continued non-payment.

Example:

A construction company in Tauranga has repeatedly tried to collect payment from a client for completed work. After sending several past due collection letters without success, the company escalates the matter by sending a formal debt collection letter, warning that the debt will be referred to a solicitor if not paid within 14 days.

Sample Formal Debt Collection Letter:

Dear [Client's Name],

We regret to inform you that your account remains unpaid despite our previous attempts to resolve the matter. As of today, your outstanding balance is $10,000 for work completed on [Date].

If payment is not received within 14 days, we will refer this matter to our solicitor for further action. This may result in additional legal fees and other charges being added to the amount owed.

We strongly encourage you to make full payment as soon as possible to avoid these additional costs.

Sincerely,

[Your Name]

[Your Company]5. Maintaining Compliance with Debt Collection Laws

When sending collection letters to customers, it’s crucial to stay compliant with New Zealand’s debt collection laws. This includes adhering to the Fair Trading Act and the Credit Contracts and Consumer Finance Act, which protect consumers from unfair practices such as harassment or misleading communications.

Best practices for compliance include:

- Avoiding aggressive or threatening language

- Providing clear and accurate information about the debt

- Offering options for dispute resolution

- Respecting requests for debt validation or cease and desist orders

6. Avoiding Common Pitfalls

Businesses must be cautious when sending collection letters to ensure that they are not crossing legal boundaries. Avoid common mistakes such as:

- Sending letters too soon (e.g., before the debt is legitimately overdue)

- Using threatening language that could be interpreted as harassment

- Failing to provide sufficient detail about the debt

- Ignoring customer requests for dispute or validation

Case Study:

A small business in Napier followed best practices by sending a collection letter to a client who had not paid for consulting services. The business kept clear documentation of all correspondence, which later helped them when the client disputed the debt. Because the business had complied with all legal requirements and maintained professionalism, they were able to successfully resolve the dispute in court.

In the next section, we will examine the role of payment collection letters, debt clearance letters, and the importance of maintaining accurate records to avoid disputes. We’ll also cover strategies for effectively closing accounts once debts are paid and ensuring that future payment issues are minimized.

Payment Collection Letters and Debt Clearance Letters

Once the debt collection process is initiated, it’s essential for businesses to manage payments effectively and confirm when debts are cleared. This helps to maintain good customer relations and ensures that the business stays compliant with New Zealand’s debt recovery laws. In this section, we’ll explore the roles of payment collection letters and debt clearance letters, how to properly close accounts after debts are settled, and the importance of maintaining accurate records throughout the process.

1. Payment Collection Letters

A payment collection letter is sent to remind a customer of their overdue balance and to prompt them to make payment. These letters are part of a broader debt collection strategy and are typically used when an account has been overdue for a moderate period. The tone of a payment collection letter can range from polite reminders to more urgent requests depending on how long the payment has been outstanding.

Example:

A local café supplier in Auckland sends a payment collection letter to a restaurant that has not paid for their last delivery of goods. The letter provides a final payment date and encourages the restaurant to settle the debt to avoid further action.

Sample Payment Collection Letter:

Dear [Customer's Name],

This is a friendly reminder that your account is overdue. The total amount of $750 for the delivery of goods on [Date] remains unpaid. We kindly request that you arrange payment by [Due Date].

Should you have any concerns about this payment or require assistance, please do not hesitate to contact us. We appreciate your prompt attention to this matter.

Thank you for your continued business.

Sincerely,

[Your Name]

[Your Company]Payment collection letters should be direct but courteous, giving the customer clear instructions on how to settle their balance. Including a payment deadline is crucial to encourage timely action, and providing options for the customer to get in touch can help resolve any misunderstandings about the debt.

2. Debt Clearance Letters

A debt clearance letter is issued once a debt has been fully paid, confirming that the account is now settled and that no further payments are required. This letter not only serves as a formal acknowledgment of payment but also helps the debtor by providing proof of the debt being cleared, which can be useful for their records or in the event of future disputes.

Debt clearance letters are especially important for maintaining transparency and protecting both parties from misunderstandings down the road. For the business, this letter serves as a final piece of documentation showing that the debt recovery process has been completed.

Example:

A debt collection agency in Wellington sends a debt clearance letter to a customer who has just paid off a long-overdue personal loan. The letter confirms that the debt has been settled and thanks the customer for their cooperation.

Sample Debt Clearance Letter:

Dear [Customer's Name],

We are pleased to confirm that your outstanding debt of $2,500 has been fully paid as of [Payment Date]. Your account is now clear, and no further payments are required.

Thank you for resolving this matter promptly. Please keep this letter for your records as proof of your payment.

Should you require any further assistance, do not hesitate to contact us.

Best regards,

[Your Name]

[Your Company]Debt clearance letters should be clear and concise, detailing the amount paid, the date of payment, and confirming that no additional payments are due. They should also include contact information in case the customer has any follow-up questions.

3. Closing Accounts After Debts Are Paid

Once a debt is paid in full, it’s important to close the account properly. This involves updating financial records to reflect that the debt has been cleared and confirming with the customer that their account is no longer active. This step is critical for maintaining accurate bookkeeping and preventing future errors, such as mistakenly sending additional payment requests to a customer who has already settled their debt.

For businesses, closing an account involves:

- Updating Records: Ensure that all internal records reflect that the debt has been paid and that the customer’s account is settled.

- Issuing Receipts: Provide the customer with a formal receipt of payment in addition to the debt clearance letter.

- Following Up: If applicable, follow up with the customer to confirm that they received the debt clearance letter and are satisfied with the resolution of the matter.

Accurate and up-to-date records are essential for avoiding disputes, especially in cases where the debt was paid after an extended period of collection efforts.

4. Importance of Maintaining Accurate Records

Keeping detailed records throughout the debt collection process is critical for businesses. These records include copies of all correspondence, such as collection letters, payment receipts, and debt clearance letters, as well as records of phone calls or emails exchanged with the customer. Proper documentation protects the business in case of future disputes or legal action.

Accurate records should include:

- Details of the Debt: The original amount, dates of service or purchase, due dates, and any interest or late fees applied.

- Collection History: Copies of all collection letters, phone call logs, emails, and responses from the customer.

- Payment Details: Receipts for all payments made, including dates, amounts, and methods of payment.

- Final Settlement: A record of the debt clearance letter and any additional correspondence confirming that the account has been closed.

By keeping detailed records, businesses can ensure compliance with New Zealand’s debt collection laws and protect themselves in the event of future disputes.

5. Resolving Disputes After Payment

Even after a debt has been paid, disputes can sometimes arise regarding the amount paid or the terms of settlement. To avoid these issues, it’s important to:

- Keep Open Communication: Stay in touch with the customer throughout the payment process to ensure that both parties agree on the amount owed and the terms of settlement.

- Issue Clear Documentation: Provide receipts and debt clearance letters to confirm that the payment has been received and the account closed.

- Be Responsive: If the customer has questions or concerns after payment, respond promptly to avoid misunderstandings or escalations.

Case Study:

A customer in Auckland disputed the amount of a debt after making payment, claiming they had been overcharged. Because the business had kept clear records of all communications, payments, and services provided, they were able to resolve the issue quickly and avoid legal action. The debt clearance letter served as proof that the account was settled, and the customer ultimately agreed that no further action was necessary.

In the next section, we will discuss the role of solicitors and attorneys in debt collection, including how they can help businesses recover unpaid debts through collection letters from attorneys and other legal means. We will also explore how businesses can escalate unresolved debts to the legal system and when it’s appropriate to involve a solicitor.

The Role of Solicitors and Attorneys in Debt Collection

When a debt remains unpaid despite multiple attempts to collect, businesses may need to involve solicitors or attorneys to escalate the situation. Legal professionals can provide a more forceful approach, using their knowledge of New Zealand’s debt collection laws to help recover outstanding debts. In this section, we will examine how collection letters from attorneys and solicitors function, when to escalate a debt to the legal system, and the steps involved in legal debt recovery.

1. Collection Letters from Attorneys

A collection letter from an attorney carries more weight than a standard debt collection letter due to the legal authority it implies. These letters often signal to the debtor that the situation has become serious and that legal action may be imminent if payment is not made promptly.

Example:

A law firm in Auckland is hired by a local construction company to send a collection letter from an attorney to a client who has refused to pay for completed services. The letter clearly states the legal consequences of failing to pay, including the potential for court proceedings.

Sample Collection Letter from Attorney:

Dear [Debtor's Name],

This letter serves as formal notice that we are representing [Your Company] in the recovery of the outstanding debt of $12,000 for services provided on [Date].

Unless full payment is received within 14 days of the date of this letter, our client will have no option but to pursue this matter through legal channels. This may result in court proceedings and additional costs being added to the total amount owed.

We urge you to make payment as soon as possible to avoid further legal action.

Sincerely,

[Attorney's Name]

[Law Firm]A letter from an attorney often prompts immediate action, as debtors are more likely to take the threat of legal action seriously. Businesses should consider using this approach when previous debt collection letters have gone unanswered, and the debt is significant enough to warrant legal involvement.

2. Escalating a Debt to the Legal System

When all other avenues have been exhausted, and the debtor still refuses to pay, businesses may need to escalate the matter to the legal system. In New Zealand, this typically involves filing a claim with the Disputes Tribunal for smaller amounts or the District Court for larger debts. Before taking this step, however, a final formal debt collection letter or debt collection notice is usually sent to the debtor, warning them of the impending legal action.

Steps in Escalating a Debt to the Legal System:

- Final Demand Letter: A formal debt collection letter or debt collection notice is sent, stating that legal action will be taken if the debt is not paid within a specified timeframe (usually 14 to 21 days).

- Filing a Claim: If the debtor fails to respond, the creditor can file a claim with the appropriate legal body. For debts under $30,000, the Disputes Tribunal is a cost-effective option. For larger amounts, the District Court may be involved.

- Court Proceedings: If the matter proceeds to court, both parties will present their case, and a judge will make a ruling. If the creditor wins, the court may order the debtor to pay the outstanding amount plus any legal fees.

- Enforcing the Judgment: If the debtor still refuses to pay after a court ruling, the creditor can seek enforcement measures such as wage garnishment or property seizure.

3. Solicitor’s Debt Collection Letters

A solicitor’s debt collection letter is similar to a collection letter from an attorney, but it may be more formal and detailed, outlining the exact legal steps that will be taken if payment is not made. Solicitors typically send these letters when previous attempts at debt collection have failed, and the situation is headed toward legal action.

Example:

A law firm in Wellington is hired by a marketing agency to send a solicitor’s debt collection letter to a client who owes $15,000 for services rendered. The letter includes a breakdown of the debt, a final deadline for payment, and a notice that court proceedings will begin if the payment is not received.

Sample Solicitor’s Debt Collection Letter:

Dear [Debtor's Name],

We are acting on behalf of [Your Company] to recover an outstanding debt of $15,000 for services provided on [Date]. Despite previous attempts to resolve this matter, payment has not been received.

This letter serves as a formal notice that unless full payment is received within 14 days, we will commence legal proceedings to recover the debt. This may include filing a claim with the District Court, which could result in additional legal costs and further action to enforce any judgment obtained.

Please consider this your final opportunity to resolve this matter before legal action is taken.

Sincerely,

[Solicitor's Name]

[Law Firm]These letters are often the last step before formal legal proceedings begin and can be effective in prompting a debtor to settle the debt without going to court.

4. Legal Collection Letters and Court Action

When a legal collection letter fails to produce payment, court action may be the only remaining option. Creditors can file a claim in the appropriate court, depending on the size of the debt, and present evidence to support their case. The court will then issue a ruling, which may include an order for the debtor to pay the outstanding amount plus any additional legal fees.

Creditors should ensure that they have all the necessary documentation to support their claim, including copies of debt collection letters, payment records, contracts, and any other relevant correspondence.

5. When to Involve a Solicitor

Involving a solicitor in debt collection is often necessary when:

- The debt is significant (typically over $10,000).

- The debtor has ignored multiple attempts to recover the debt.

- The situation has become contentious, and legal advice is needed to navigate the complexities.

- The business prefers to take a more formal, legally binding approach to recover the debt.

A solicitor can provide valuable guidance on the best course of action, from drafting legal notices to representing the business in court if necessary. They can also help ensure that all communications and actions comply with New Zealand’s debt collection laws, protecting the business from potential legal pitfalls.

6. Understanding Legal Costs and Risks

It’s important for businesses to weigh the costs and risks associated with escalating a debt to the legal system. Legal fees, court costs, and the time involved in pursuing a claim can add up, and there is no guarantee that the debtor will be able to pay even if a judgment is obtained.

Considerations before Escalation:

- Cost of Legal Action: Is the debt large enough to justify the legal costs involved in pursuing it?

- Likelihood of Recovery: Does the debtor have the means to pay if a court judgment is obtained?

- Impact on Business Relations: Will pursuing legal action harm the business relationship or reputation?

Businesses should carefully consider these factors before deciding to escalate a debt to the legal system.

In the next section, we will discuss strategies for businesses to prevent debts from becoming overdue in the first place. This includes implementing effective invoicing practices, offering payment plans, and using automated systems to track accounts receivable. We will also explore how businesses can build strong customer relationships to reduce the likelihood of late payments and disputes.

Preventing Debts from Becoming Overdue

While debt collection letters and legal actions are necessary steps when debts go unpaid, the ideal approach for businesses is to prevent debts from becoming overdue in the first place. Implementing proactive strategies can significantly reduce the need for debt collection letters and help businesses maintain healthy cash flow while preserving positive relationships with their clients.

In this section, we will explore practical methods for preventing overdue debts, including effective invoicing practices, offering payment plans, and utilizing technology to manage accounts receivable. Additionally, we will discuss how building strong customer relationships can help businesses minimize the risk of late payments and disputes.

1. Effective Invoicing Practices

The invoicing process is the foundation of debt prevention. By implementing clear and efficient invoicing practices, businesses can ensure that customers understand their payment obligations and are more likely to pay on time.

Best Practices for Invoicing:

- Timely Invoicing: Send invoices promptly upon completion of work or delivery of goods. Delaying invoices can lead to confusion and increase the likelihood of late payments.

- Clear Payment Terms: Clearly state the payment terms on the invoice, including the due date, accepted payment methods, and any penalties for late payment.

- Detailed Breakdown: Provide a detailed breakdown of the services or products provided, along with the corresponding costs. This reduces the chance of disputes over the amount owed.

- Automatic Reminders: Set up automated reminders to notify customers of upcoming payment due dates, as well as follow-ups for overdue accounts.

Example:

A graphic design agency in Auckland ensures that all invoices are sent within 24 hours of project completion. Their invoices clearly outline the services provided, the total amount due, and the payment deadline. They also use software that automatically sends payment reminders to clients seven days before the invoice is due.

2. Offering Payment Plans

For customers facing financial difficulties, offering payment plans can be a helpful way to prevent debts from becoming overdue. A well-structured payment plan allows the customer to pay off their debt over time while ensuring that the business continues to receive payments regularly.

How to Structure a Payment Plan:

- Initial Payment: Require an upfront payment to ensure that the customer is committed to settling their debt.

- Installments: Break down the total debt into manageable installments that the customer can pay over a set period (e.g., monthly or bi-weekly payments).

- Interest or Fees: Consider adding a small interest rate or administrative fee to cover the costs of managing the payment plan.

- Written Agreement: Have both parties sign a written agreement outlining the terms of the payment plan, including the payment schedule, total amount due, and any penalties for missed payments.

Example:

A car repair shop in Christchurch offers customers the option to pay large repair bills in monthly installments. They work with customers to create payment plans that fit their budgets and ensure that payments are made regularly, preventing the need for debt collection letters.

3. Using Automated Systems for Accounts Receivable

Managing accounts receivable manually can be time-consuming and prone to errors. By using automated systems, businesses can streamline the process of tracking outstanding invoices, sending reminders, and even flagging accounts that are at risk of becoming overdue.

Benefits of Automation:

- Efficiency: Automated systems can send invoices and reminders, reducing the administrative burden on staff.

- Accuracy: These systems reduce the likelihood of errors in invoicing and payment tracking.

- Real-Time Insights: Automated software provides real-time updates on which accounts are overdue, allowing businesses to act quickly before debts become problematic.

Example:

An accounting firm in Wellington uses an automated invoicing system that tracks all outstanding accounts and sends follow-up emails to clients with overdue invoices. The system also generates reports that help the firm identify patterns of late payment and take preemptive action with certain clients.

4. Strengthening Customer Relationships

Building strong relationships with customers can go a long way in reducing the likelihood of late payments. When customers value the relationship with a business, they are more likely to prioritize payments and communicate openly if they encounter financial difficulties.

Strategies for Building Relationships:

- Regular Communication: Maintain open and regular communication with customers, especially during long-term projects or ongoing services.

- Customer Service: Offer excellent customer service to resolve any issues or concerns that could lead to payment disputes.

- Personalized Attention: Tailor your services and communication to meet the unique needs of each customer, making them feel valued and appreciated.

Example:

A landscaping company in Napier has a dedicated customer service team that checks in with clients regularly to ensure they are satisfied with the work being done. This proactive communication helps address any concerns early on and ensures that clients are more willing to pay on time.

5. Setting Clear Expectations Upfront

One of the most effective ways to prevent overdue debts is to set clear expectations from the start of the business relationship. Before work begins or products are delivered, both parties should agree on the payment terms, deadlines, and any penalties for late payment. This helps prevent misunderstandings and ensures that the customer knows exactly what is expected of them.

Key Elements to Include in an Agreement:

- Payment Terms: Clearly outline the payment terms, including the due date and any applicable late fees.

- Scope of Work: Ensure that both parties agree on the scope of work or products to be provided, as this can prevent disputes over the final invoice.

- Penalties: Include a clause that explains the penalties for late payment, such as interest charges or collection fees.

Example:

A home renovation company in Dunedin provides all clients with a written agreement before starting work. The agreement includes the payment terms, project timeline, and a breakdown of costs. Both the client and the company sign the agreement to confirm their understanding and commitment to the terms.

6. Early Intervention with Gentle Reminders

When a payment is approaching or has just become overdue, gentle reminders can be effective in prompting customers to take action. Often, customers simply forget to pay on time, and a polite reminder is all that is needed to resolve the situation.

Example:

A small IT services company in Tauranga sends a friendly email reminder to clients when their invoice is 7 days overdue. The email is polite and non-confrontational, reminding the client to settle the bill without escalating the matter unnecessarily.

Sample Gentle Reminder Email:

Dear [Client's Name],

We hope this message finds you well. This is a friendly reminder that your invoice for [Service Provided] is now overdue by 7 days. We would greatly appreciate it if you could arrange payment at your earliest convenience.

If you have already made the payment, please disregard this message. Should you have any questions or need assistance, feel free to contact us.

Thank you for your attention to this matter.

Best regards,

[Your Name]

[Your Company]7. Offering Discounts for Early Payment

To incentivize customers to pay early, businesses can offer small discounts for payments made before the due date. This can be an effective strategy to encourage prompt payment and reduce the risk of overdue accounts.

Example:

A supplier in Hamilton offers clients a 2% discount if they pay their invoice within 10 days of receiving it. Many clients take advantage of the discount, resulting in faster payments and fewer overdue accounts.

In the next section, we will explore additional methods businesses can use to handle customers who are consistently late on payments, including how to implement credit policies and when it might be necessary to stop providing services until the account is settled. Additionally, we will discuss ways to protect the business’s cash flow by leveraging credit checks and risk management practices.

Handling Consistently Late Payments and Managing Credit Risk

While proactive measures like effective invoicing and maintaining strong customer relationships can reduce the likelihood of overdue debts, there are always some customers who are consistently late with payments. For these customers, it’s crucial to have clear policies in place and to manage the risks associated with offering credit. In this section, we will explore how businesses can handle late-paying customers, implement credit policies, and protect cash flow through credit checks and risk management practices.

1. Identifying Consistently Late-Paying Customers

The first step in dealing with consistently late-paying customers is identifying them. By keeping detailed records of payment histories, businesses can track patterns of late payments and take action accordingly. Monitoring accounts receivable and identifying repeat offenders allows businesses to create tailored strategies to deal with these customers.

Steps to Identify Late-Paying Customers:

- Track Payment History: Use accounting software or automated systems to track when invoices are paid and whether they are consistently late.

- Categorize Customers: Categorize customers based on their payment behaviors, such as “on-time payers,” “occasional late payers,” and “chronic late payers.”

- Monitor Communication: Keep records of communication with customers about late payments, including reminders, phone calls, and collection letters.

Example:

A wholesaler in Auckland uses an automated invoicing system that tracks the payment history of each client. By analyzing the data, the business identifies a few clients who consistently pay late. They adjust their approach to managing these accounts by tightening payment terms and communicating more frequently.

2. Implementing Credit Policies

Establishing clear credit policies is a key component of managing late-paying customers. Credit policies set the rules for extending credit to customers and outline the consequences for late payment. A well-defined credit policy ensures that customers understand their obligations and helps protect the business from financial risk.

Elements of a Credit Policy:

- Credit Terms: Define the payment terms, such as “net 30” or “net 60,” meaning payment is due within 30 or 60 days of the invoice date.

- Credit Limits: Set limits on the amount of credit extended to customers based on their financial stability and payment history.

- Late Payment Penalties: Include clear penalties for late payments, such as interest charges or late fees. Make sure these penalties comply with New Zealand laws.

- Review Process: Regularly review and update credit policies to ensure they remain aligned with the business’s needs and market conditions.

Example:

A furniture supplier in Christchurch establishes a credit policy that requires new customers to pay upfront for their first few orders. After building a positive payment history, customers can apply for credit with terms of “net 30.” The policy also includes a 5% late fee for payments that are more than 10 days overdue.

3. Offering Incentives for Early Payment

As discussed earlier, offering discounts for early payment is a proven strategy for encouraging customers to pay promptly. This practice not only reduces the likelihood of late payments but also improves cash flow. Businesses should weigh the cost of the discount against the benefit of receiving payments earlier.

Example:

A printing company in Wellington offers a 2% discount for clients who pay their invoices within 10 days of receipt. This incentive encourages clients to pay earlier, significantly reducing the number of overdue accounts.

4. When to Stop Providing Services

For customers who are consistently late with payments, it may become necessary to stop providing services or delivering products until their accounts are settled. This is often a last resort but can be an effective way to protect the business from further financial loss.

Steps to Stop Services:

- Communicate Clearly: Inform the customer that services or product deliveries will be halted until the outstanding balance is paid.

- Provide a Final Deadline: Set a final deadline for payment and clearly state that services will be resumed only once payment is received.

- Document the Process: Keep detailed records of all communication with the customer regarding the stoppage of services to protect the business from disputes.

Example:

A software development company in Dunedin has a client who consistently fails to pay on time. After multiple late payments, the company informs the client that no further work will be completed on their project until the outstanding balance is paid. The client quickly settles the account to resume the project.

5. Using Credit Checks to Minimize Risk

Before extending credit to new customers, it’s important to assess their financial stability and creditworthiness. Credit checks help businesses evaluate the risk of offering credit and avoid customers who may be unable or unwilling to pay on time.

Benefits of Credit Checks:

- Risk Assessment: Determine whether a customer is likely to pay on time based on their credit history.

- Informed Decision-Making: Make informed decisions about how much credit to extend or whether to offer credit at all.

- Avoiding Bad Debts: Minimize the risk of bad debts by choosing to work only with customers who have a solid credit history.

Example:

A construction materials supplier in Hamilton runs credit checks on all new clients before agreeing to provide materials on credit. By doing so, they avoid working with clients who have a history of defaulting on payments, protecting their business from potential losses.

6. Monitoring Accounts Receivable and Cash Flow

Regularly monitoring accounts receivable is essential to managing credit risk and ensuring that cash flow remains stable. Businesses should have a system in place to track outstanding invoices, identify overdue accounts, and prioritize collection efforts.

Best Practices for Monitoring Accounts Receivable:

- Automated Tracking: Use software to automate the tracking of invoices and alert you when accounts become overdue.

- Aging Reports: Generate aging reports to categorize outstanding invoices by how long they have been overdue (e.g., 30, 60, 90 days).

- Regular Reviews: Review accounts receivable regularly to stay on top of potential issues before they escalate.

Example:

A healthcare equipment supplier in Auckland generates aging reports every week to monitor overdue accounts. They prioritize contacting clients with the oldest outstanding balances to encourage prompt payment and maintain healthy cash flow.

7. Working with a Debt Collection Agency

If a customer continues to fail to pay despite multiple reminders and interventions, it may be necessary to work with a debt collection agency. Debt collection agencies specialize in recovering overdue payments and can be particularly helpful when the debt is significant, or the customer is unresponsive.

How to Choose a Debt Collection Agency:

- Reputation: Choose an agency with a strong reputation for ethical practices and successful debt recovery.

- Industry Experience: Select an agency that has experience working with businesses in your industry.

- Fee Structure: Understand the agency’s fee structure and how much they will charge for successful recovery.

Example:

A manufacturer in Nelson decides to hire a debt collection agency after a client fails to pay a $20,000 invoice for several months. The agency successfully recovers the debt, allowing the manufacturer to focus on their core business operations.

In the next section, we will discuss the process of writing effective debt collection letters for customers who have become overdue. We will explore different templates, tones, and strategies to ensure that these letters are both professional and effective in recovering payments. We will also look at how to escalate letters when initial attempts are unsuccessful, ensuring that businesses have a structured approach to collecting overdue debts.

Writing Effective Debt Collection Letters

Debt collection letters are essential tools for businesses when customers fail to pay on time. These letters should be professional, clear, and concise, communicating the seriousness of the overdue payment while maintaining a respectful tone. The structure and content of a debt collection letter can vary depending on the stage of the collection process, from initial gentle reminders to more assertive demands for payment.

In this section, we will explore different types of debt collection letters, provide templates for each stage of the process, and offer tips on how to escalate your approach if payment is not received. Writing effective debt collection letters will help your business recover overdue payments while staying compliant with New Zealand laws.

1. Initial Gentle Reminder Letter

The first step in the debt collection process is sending a gentle reminder to the customer. This letter is typically sent shortly after the payment due date has passed and assumes that the late payment may be an oversight on the customer’s part. The tone should be friendly and non-confrontational, simply reminding the customer of the overdue payment and providing instructions on how to settle the account.

Example:

A web development agency in Wellington sends an initial gentle reminder to a client who is five days late on paying their invoice for website maintenance services.

Sample Initial Gentle Reminder Letter:

Subject: Friendly Reminder – Invoice Overdue

Dear [Client's Name],

We hope this message finds you well. This is just a friendly reminder that your invoice for [Service Provided] dated [Invoice Date] is now past due by [X] days. The total amount due is [Amount].

We kindly request that you arrange payment at your earliest convenience. If you have already made the payment, please disregard this notice. Should you have any questions or need assistance, please don't hesitate to contact us.

Thank you for your prompt attention to this matter, and we appreciate your continued business.

Best regards,

[Your Name]

[Your Company]

[Contact Information]This type of letter is ideal for customers who usually pay on time but may have overlooked an invoice. It serves as a polite nudge to remind them of their obligation.

2. Formal Payment Collection Letter

If the gentle reminder goes unanswered and the payment is still not received, a more formal payment collection letter should be sent. This letter takes on a firmer tone and outlines the consequences of continued non-payment. It may also mention any late fees or penalties that will be applied if the payment is not made promptly.

Example:

A marketing firm in Auckland sends a formal payment collection letter to a client who has not paid for a digital advertising campaign after 30 days.

Sample Formal Payment Collection Letter:

Subject: Overdue Payment – Immediate Action Required

Dear [Client's Name],

We are writing to inform you that your payment for invoice [Invoice Number], dated [Invoice Date], is now [X] days overdue. The total amount outstanding is [Amount], and we have yet to receive your payment.

Please be aware that failure to settle this account within the next [Number of Days] will result in a late fee of [Fee Amount] being added to your balance. To avoid any additional charges, we kindly request that you arrange payment immediately.

If you have already processed this payment, please let us know so we can update our records. Otherwise, please contact us if you need to discuss alternative payment arrangements.

Thank you for your prompt attention to this matter.

Sincerely,

[Your Name]

[Your Company]

[Contact Information]This letter is appropriate when the customer has already been given a gentle reminder, and it is clear that stronger action is needed. It should clearly communicate the consequences of non-payment, such as late fees, without being overly aggressive.

3. Final Demand Letter

When previous attempts to collect the debt have failed, a final demand letter should be sent. This letter is more urgent and assertive, warning the customer that if the payment is not made within a specified time frame, the debt will be escalated to a collection agency or legal action. The final demand letter serves as the last step before taking more formal action.

Example:

A construction company in Christchurch sends a final demand letter to a client who has ignored previous payment reminders and owes a significant amount for completed work.

Sample Final Demand Letter:

Subject: Final Demand for Payment – Legal Action Pending

Dear [Client's Name],

This is to inform you that despite our previous reminders, your payment for invoice [Invoice Number], dated [Invoice Date], remains outstanding. The total amount due is [Amount], and it is now [X] days overdue.

Please be advised that unless full payment is received within [Number of Days], we will have no choice but to escalate this matter to a debt collection agency or initiate legal proceedings. This may result in additional costs being added to your account, which you will be responsible for.

To avoid these further actions, we strongly urge you to settle your account immediately.

If you have already made payment, please contact us to confirm so we can update our records. We are still open to discussing any payment difficulties you may be experiencing, but this matter must be resolved without delay.

Sincerely,

[Your Name]

[Your Company]

[Contact Information]The final demand letter is a serious communication, and it should make clear that this is the last opportunity to resolve the debt before more aggressive measures are taken. This letter may also serve as evidence if the matter is taken to court.

4. Escalating the Letter to Legal Collection

If the final demand letter fails to elicit payment, the next step may be to involve a solicitor or debt collection agency. A legal collection letter can be sent from the solicitor’s office, emphasizing the legal ramifications of non-payment. This letter carries significant weight as it signals that the creditor is ready to take formal legal action.

Example:

A solicitor in Dunedin sends a legal collection letter on behalf of a client who has been unable to recover a debt from a non-paying customer.

Sample Legal Collection Letter:

Subject: Notice of Legal Action – Immediate Payment Required

Dear [Debtor's Name],

We are writing on behalf of our client, [Your Company], regarding the outstanding balance of [Amount] for services provided on [Date]. Despite multiple attempts to resolve this matter, payment has not been received.

Please be advised that unless the full balance is paid within [Number of Days], we will proceed with filing legal action to recover the debt. This action may include seeking a court judgment against you, which could result in additional costs and legal fees being added to your debt.

We strongly recommend that you contact our office immediately to arrange payment and avoid these consequences.

Sincerely,

[Solicitor's Name]

[Law Firm Name]

[Contact Information]This letter clearly outlines the legal actions that will be taken if the debtor does not pay, including court proceedings and the addition of legal fees. At this point, the debtor is usually more motivated to settle the debt to avoid the legal consequences.

5. Tips for Writing Effective Debt Collection Letters

- Be Clear and Specific: Always state the exact amount owed, the original invoice date, and the deadline for payment.

- Professional Tone: Maintain a professional and respectful tone, even when the letter is more urgent.

- Offer Solutions: In the earlier stages, provide options for payment plans or extended deadlines to encourage resolution.

- Legal Compliance: Ensure that all debt collection letters comply with New Zealand’s debt collection laws to avoid any legal repercussions for the business.

6. Escalating Your Approach

The escalation process should be methodical and follow a clear timeline:

- Gentle Reminder: Sent a few days after the due date.

- Formal Payment Collection Letter: Sent if no payment is received after the reminder.

- Final Demand Letter: Sent when the debt is seriously overdue.

- Legal Collection Letter: Sent if the debtor continues to ignore previous communications.

Case Study:

A printing company in Auckland followed the above escalation process for a customer who had failed to pay a $5,000 invoice. After sending a final demand letter, the customer contacted the business and agreed to a payment plan, avoiding further legal action. The structured approach ensured that the business remained professional while recovering the debt.

In the next section, we will look at case studies that highlight successful debt recovery through effective use of debt collection letters, as well as strategies for improving future payment behaviors among customers. These case studies will illustrate how businesses in New Zealand can implement structured processes for debt recovery and minimize future unpaid debts.

Take the Guesswork Out of Writing Debt Collection Letters

Writing effective debt collection letters can be time-consuming and complex. To help streamline this process, we offer a free tool that guides businesses through creating professional and compliant debt collection letters, including first reminders, second notices, and final demand letters. Try our free tool here to simplify your debt recovery efforts and get paid faster.

Case Studies in Successful Debt Recovery

The use of debt collection letters is a common and effective method for recovering overdue payments, but the approach must be tailored to the specific situation. In this section, we will examine real-world case studies from New Zealand businesses that have successfully recovered debts through structured use of debt collection letters. These examples will highlight strategies that businesses can adopt to improve their debt recovery processes and minimize the likelihood of future unpaid debts.

Case Study 1: Recovering Debt with a Formal Payment Plan

Business: An accounting firm in Auckland

Debt Amount: $12,000

Industry: Professional Services

Situation:

The accounting firm had been providing bookkeeping services to a client for over a year. The client had accrued a debt of $12,000 for services rendered but had failed to pay on time for several consecutive months. The accounting firm sent an initial gentle reminder letter, followed by a more formal payment collection letter. Despite these efforts, no payment was received.

Actions Taken:

The firm escalated the situation by sending a final demand letter that clearly outlined the next steps, including the possibility of involving a solicitor if payment was not made. Along with this letter, the firm offered the client an option to set up a payment plan to avoid legal action.

Outcome:

The client responded to the final demand letter and agreed to a payment plan that allowed them to pay off the debt over six months. The accounting firm was able to recover the full amount without needing to escalate the matter further to legal action.

Key Takeaways:

- Offering a payment plan as an option in the final demand letter provided a resolution that benefited both the client and the business.

- The structured escalation of debt collection letters showed professionalism and a willingness to negotiate, resulting in a positive outcome.

Case Study 2: Using Legal Collection Letters for Stubborn Debtors

Business: A construction company in Christchurch

Debt Amount: $25,000

Industry: Construction

Situation:

A large project had been completed for a client, but the construction company was struggling to collect $25,000 in final payments. The client repeatedly ignored emails, calls, and multiple debt collection letters. The debt was already 90 days overdue when the construction company decided to escalate the issue.

Actions Taken:

After sending a final demand letter with no response, the company hired a solicitor to issue a legal collection letter. The letter threatened legal action and outlined the potential consequences of a court judgment, including legal fees and damage to the client’s credit rating.

Outcome:

The legal threat was enough to prompt the client to make contact and settle the full amount within two weeks. The business was able to avoid court proceedings and recover the debt without further complications.

Key Takeaways:

- The involvement of a solicitor added weight to the collection process and demonstrated the company’s seriousness.

- Escalating to a legal collection letter was a decisive action that resulted in prompt payment.

Case Study 3: Resolving Small Debts with Clear Communication

Business: A freelance web designer in Wellington

Debt Amount: $1,500

Industry: Digital Services

Situation:

A small business client had failed to pay for website updates totaling $1,500. Despite sending a gentle reminder letter and a formal payment collection letter, the client did not respond. The web designer was reluctant to involve a solicitor due to the small amount of the debt but needed to resolve the issue to avoid financial strain.

Actions Taken:

The web designer sent a final demand letter but took a different approach by offering a 10% discount if the client paid within the next seven days. This offer was made as a gesture of goodwill and to avoid further escalation.

Outcome:

The client paid the discounted amount within the deadline, allowing the web designer to close the account and avoid the stress of pursuing further action.

Key Takeaways:

- Offering a discount as a final attempt to settle the debt can be an effective strategy, especially for smaller amounts.

- Maintaining a flexible approach while still being firm helped the business recover the payment without damaging the relationship.

Case Study 4: Managing Ongoing Late Payments with Preventative Measures

Business: A wholesale supplier in Hamilton

Debt Amount: $8,000

Industry: Wholesale/Retail

Situation:

The wholesale supplier had been dealing with a retail client who consistently paid late. Over time, the client had accrued $8,000 in overdue invoices. The supplier had sent multiple collection letters, and although the client eventually paid, they continued to delay payments with every new order.

Actions Taken:

The supplier decided to implement stricter payment terms and credit policies for the client. They reduced the client’s credit limit and required partial payment upfront for future orders. They also introduced a penalty for late payments in their updated contract.

Outcome:

The client began making payments on time to avoid the penalties and to ensure they could continue receiving wholesale products. The new credit policy helped prevent further late payments while maintaining the business relationship.

Key Takeaways:

- Implementing stricter credit terms and upfront payment requirements can help businesses manage clients who are habitually late.

- Proactively adjusting credit policies can protect the business’s cash flow while still offering clients the flexibility to continue working together.

Case Study 5: Escalating to a Debt Collection Agency

Business: A gym in Auckland

Debt Amount: $2,500

Industry: Fitness Services

Situation:

The gym had several members who had failed to pay their membership fees for several months, resulting in a combined debt of $2,500. The gym sent multiple debt collection letters but received no response from the members. After multiple failed attempts to recover the payments, the gym decided to escalate the matter.

Actions Taken:

The gym hired a debt collection agency to pursue the unpaid fees. The agency sent legal collection letters to each member, outlining the consequences of non-payment and the legal actions that could follow if the debt was not settled.

Outcome:

Within one month, the agency was able to recover the majority of the unpaid fees. The gym regained its lost revenue without having to personally handle the collection process.

Key Takeaways:

- Partnering with a debt collection agency is an effective solution when internal efforts fail to recover debts.

- Outsourcing the debt recovery process can save time and resources, allowing the business to focus on its core operations.

Strategies for Preventing Future Payment Issues

The case studies above demonstrate how businesses can use structured debt recovery processes to successfully collect unpaid debts. However, the ultimate goal for any business is to reduce the number of overdue payments in the first place. Below are strategies to help prevent future payment issues:

1. Clear Contracts and Agreements